[ad_1]

Trading 33% off its highs, Tyson Foods TSN fiscal Q4 earnings on November 14 will tell Wall Street if the meat giant is gaining steam or struggling with higher operating costs.

Tyson’s report will also provide insights into large food retailers to see if they were able to profit from rising inflation amid an economic downturn as more consumers stick to the essentials.

Basics & Trends

Historically investors have sought out food companies like Tyson Foods during challenging economic times and market uncertainty for defensive protection. The nearby chart shows that industry competitor Hormel Foods HRL total return has climbed over the last year, while TSN shares have lagged the S&P 500. Let’s see why Tyson might not be holding up and acting as defensive as one might assume.

Image Source: Zacks Investment Research

Tyson Foods is the largest U.S. producer of chicken and is a leader in protein as a whole, with offerings across beef, pork, and prepared foods. Even though meat prices soared along with rising inflation, Tyson Foods has not been able to fully capitalize on rising commodities because of their own rising costs and other headwinds.

TSN reached highs of $100.72 per share in February after posting record profits from its beef business last year. Profits have declined this year with the company struggling to meet demand in chicken production. Tyson Foods has faced labor shortages, along with higher labor costs.

Last quarter, President and CEO Donnie King said improving chicken supply is one of the biggest issues facing the company, with Tyson Foods estimated to provide a fifth of the nation’s chicken production. The company struggled to fulfill orders due to limitations on supplies and labor. Investors will be hoping the operator of famous food brands such as Jimmy Dean and Hillshire Farm was able to improve on this during the quarter and help lift its outlook.

Outlook

The Zacks Consensus Estimate for TSN’s fiscal Q4 earnings is $1.70 per share, which would be a decline of -26% from Q4 2021. Earnings estimates for the period have gone down from $1.77 at the beginning of the quarter. Sales for Q4 are expected to climb 4% at $13.29 billion. This is an indication that operating costs are weighing on TSN’s profits.

Year over year, TSN earnings are expected to rise 6% but decline -22% in FY23 at $6.88 per share. Sales are expected to be up 12% this year and be virtually flat in FY23 at $52.60 billion.

Performance & Valuation

TSN is down -22% YTD to underperform the S&P 500’s -18% and roughly match its peer group’s -20% decline. Over the last decade, TSN is up an impressive +372% when including its dividend to beat the benchmark and its peer group’s +135%.

Image Source: Zacks Investment Research

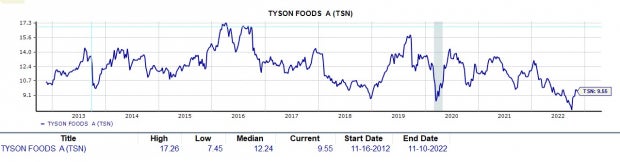

Trading around $67 a share, TSN trades at 9.6X earnings. This is near the industry average P/E of 8.7X. TSN trades below its decade-high of 17.2X and the median of 12.2X. The stock trades attractively relative to its past but FY23 earnings are expected to decline significantly with estimate revisions also trending down over the last 90 days.

Image Source: Zacks Investment Research

Bottom Line

TSN lands a Zacks Rank #4 (Sell) in correlation with declining earnings estimate revisions. Tyson Foods stock trades reasonably when considering its past, but a strong Q3 report and even stronger guidance will likely be crucial for the stock. TSN has consistently beat the Zacks Consensus but its most accurate Zacks estimate comes in well below the current consensus, indicating that it could fall short of expectations.

The Tyson Foods report should also provide another perspective on the effect inflation had on consumer spending with big omnichannel retailers like Walmart WMT and Target TGT reporting next week as well.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock And 4 Runners Up

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Hormel Foods Corporation (HRL): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

[ad_2]

Image and article originally from www.nasdaq.com. Read the original article here.