[ad_1]

Market volatility this year may have some investors looking to rebalance their portfolios. When buying stocks, one might often look for companies that appear to be trading at discounts.

Ashford Inc. AINC stock is worthy of consideration for those looking for a discount. AINC currently sports a Zacks Rank #1 (Strong Buy) with earnings estimate revisions trending higher. The Financial-Investment Management Industry is also in the top 39% of all Zacks Industries. Even better, AINC has an overall “A” VGM grade for its combined Style Score of Value, Growth, and Momentum.

Company Overview

Ashford Inc. provides asset management among other services to companies in the hospitality industry. The company manages real estate, hospitality, and securities platforms. Ashford is the advisor to two real estate investment trusts (REITs), Ashford Hospitality Trust (Ashford Trust) and Ashford Hospitality Prime (Ashford Prime).

After completing a spinoff from Ashford Hospitality Trust, Inc. AHT in November 2014, AINC began trading as its own stand-alone company.

Outlook

Year over year, AINC earnings are expected to climb 22% in 2022 at $6.36 per share. This is up from $5.60 a share 90 days ago. Fiscal 2023 earnings are expected to decline -10% after an impressive and tough-to-follow year. However, FY23 earnings estimates have also gone higher to $5.73 per share from $5.20 last quarter.

Top line growth is expected, with sales set to jump 64% in 2022 to $636.70 million compared to $388.48 million in 2021. FY23 sales are expected to rise another 11%.

Performance & Valuation

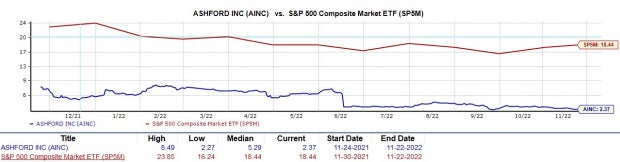

Since its split from Ashford Trust, AINC is down -77% to underperform the benchmark and its Zacks Subindustry’s -18%. But past performance is no guarantee of the future. Year to date, AINC is down -13% to slightly outperform the S&P 500’s -17%. This has also outperformed the Financial-Investment Management Markets -18%.

The stock has climbed roughly 7% in Q4. And AINC might look like a bargain as it still trades 37% from its highs of $23.60 per share seen around this time last November.

Image Source: Zacks Investment Research

With that being said, the stock is starting to look undervalued at current levels when considering its earnings potential. Trading at $14 per share AINC has a forward P/E of 2.1X, well below the industry average of 10.8X.

AINC trades at a significant discount to its historic high of 184.7X and the median of 5.5X. Even better and more recently, AINC has traded nicely below its high over the last year of 8.4X and the median of 5.2X.

Image Source: Zacks Investment Research

Bottom Line

AINC stock could be poised to go higher considering its earnings potential and low valuation. Rising earnings estimate revisions is also a good sign and could be a catalyst for the stock. At its current levels, the Average Zacks Price Target suggests 69% upside.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Ashford Inc. (AINC): Free Stock Analysis Report

Ashford Hospitality Trust Inc (AHT): Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

[ad_2]

Image and article originally from www.nasdaq.com. Read the original article here.