[ad_1]

This raging inflation will keep dishing up a lot more surprises.

By Wolf Richter for WOLF STREET.

On Sunday at the Mortgage Bankers Association Annual Convention & Expo in Nashville, the MBA’s chief economist Mike Fratantoni forecast that by the end of 2023, the average 30-year fixed mortgage rate would drop to 5.4%. And this made some headlines in the news.

In its regular monthly forecast, the MBA predicted the same: Mortgage rates would drop to 5.4% by the end of 2023. But it also forecast that mortgage rates, which are now around 7%, will drop to 6.2% by the end of March 2023, and will then continue dropping for the rest of the year until they reach 5.4% at the end of 2023.

But wait a minute… In October 2021, exactly a year ago, the MBA forecast that the average 30-year fixed mortgage rate would be 4% by Q4 2022, which is right now. And right now mortgage rates are 7%.

It was and remains just incomprehensible to the mortgage industry that mortgage rates could actually go back to what used to be the old normal before QE. And wishful thinking sets in.

Along with many others, the MBA is forecasting a recession for the first half next year, or at least the good folks there are hoping for a recession by then, because they’re hoping that a recession would bring down mortgage rates, because the surge in mortgage rates this year has crushed and battered the mortgage bankers’ business.

The mortgage industry makes its revenues from writing mortgages and then selling the mortgages to Fannie Mae, Freddie Mac, and other financial institutions that then securitize the mortgages into MBS. And those revenues have collapsed.

There have been mass-layoffs across mortgage lenders, some of the bigger ones are teetering, and some smaller ones already shut down or filed for bankruptcy. The stocks of the biggest mortgage lenders have collapsed from their highs by 79% (United Wholesale Mortgage), by 85% (Rocket Companies, former Quicken Loans, the #1 mortgage lender in the US), and by 96% (Loandepot), and they’re all featured in my Imploded Stocks. For more on the plight of this industry, read Mortgage Lender Woes.

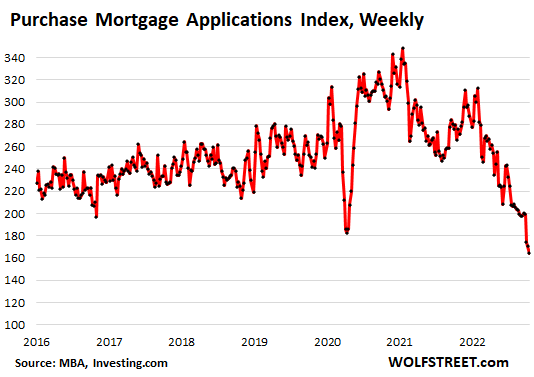

The mortgage refinance business has collapsed by 85% from a year ago, to the lowest level since the year 2000, according to mortgage applications data from the MBA, because hardly anyone would be refinancing a 3% mortgage into a 7% mortgage, except to pull out cash, and then sell the home asap.

And the business of writing mortgages to purchase a home has plunged by 35% from the still gloriously heady days a year ago:

So praying for a recession, and hoping that the recession will cause the Fed to relent and cut interest rates and end this horrible cruel QT, and start buying MBS and do QE all over again to bring down mortgage rates, while inflation is tearing up the economy, is the logical thing to pray for, if your industry is getting battered by collapsing revenues.

“The upside of that [recession] potentially for the industry is, that’s the thing that’s likely going to bring rates down a little bit,” Fratantoni said, as reported by MarketWatch.

“Mortgage rates will drop as the global economy slows, settle at 5.4% by the end of 2023,” a slide in his presentation said.

The average 30-year fixed mortgage rate is 7.29% today, according to the daily measure by Mortgage News Daily. The weekly measures from Freddie Mac and the MBA last week rose to 6.94%, over twice the rate a year ago.

“We are holding to our view that this is a spike right now, driven by financial-market dislocation, heightened level of volatility in the market and this global slowdown we’re about to experience, the likelihood of recession in the U.S. will begin to pull this number,” Fratantoni said.

Forget about this raging inflation just to save the revenues and profits of this industry?

So mortgage rates would have to drop by 1.6 percentage points from around 7% now to 5.4% by the end of 2023, according to the MBA.

But a year ago, the MBA allowed its wishful thinking to dominate its forecast. At the time, inflation was already spiking, and CPI had blown through the 6% line and was shooting straight up, and the Fed had had its infamous pivot where it started taking inflation seriously. And the MBA still forecast 4% mortgage rates for Q4 2022. Because reality would have been too painful to bear.

And this inflation has dished up lots of surprises. Inflation in some goods is backing off, but inflation is now spiking in services, where it is a lot stickier than in goods and very difficult to dislodge, and services is where consumers do nearly two-thirds of their spending. The CPI for services spiked for the 13th month in a row, by 0.7% in September from August, and by 7.4% year-over-year, the worst increase since 1982.

Anyone forecasting anything in this environment of raging inflation is going to be waylaid by surprises. This inflation has spent the past 20 month dishing up lots of nasty surprises, and there are likely a lot more to come. And mortgage rates don’t exist in a universe of their own without inflation.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Image and article originally from wolfstreet.com. Read the original article here.