[ad_1]

US Stock Market Key Points:

- The S&P 500, Dow, and Nasdaq 100 had a volatile start to the day and finished higher despite the largest ever rate hike from the ECB.

- Fed Chairman Powell reiterates hawkish statements with regards to fighting inflation.

- All eyes on US CPI next week and then the FOMC the week after.

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

Most Read: ECB Delivers Unprecedented 75bps Hike to Dampen Record Inflation, EURUSD Fades

At the open, US equity indices fell to negative territory following Fed Chairman Powell’s remarks, in which he reiterated the Central Bank’s commitment to addressing inflation, just as he did during the Jackson Hole Economic Symposium.

Speaking at the Cato Institute, an American think tank, Powell reaffirmed the independence of the institution but also reiterated the Fed’s responsibility for price stability. Powell noted that the FOMC has not finished its job of reducing inflation, as wages remain elevated while the labor market continues to be extraordinarily strong. And on this note, unemployment claims for the week ending on September 3rd surprised to the upside by reaching the lowest levels since May.

The immediate market reaction to Powell’s hawkish comments was as expected. US Treasury yields rose, the US dollar strengthened and risk assets such as equities fell into negative territory. But as the session progressed, bulls and bears fought for control with buyers gaining a slight edge through the session.

Bulls seemingly shrugged off the prospect of rising interest rates despite other Fed officials commenting on the need to keep inflation expectations in check with restrictive policy.

Earlier in the morning, the ECB delivered an expected 75-basis point rate increase to fight soaring inflation. During the press conference, ECB President Lagarde conveyed a hawkish stance and despite failing to give a clear guidance on future interest rate hikes, ECB officials did not rule out further aggressive measures to bring inflation back towards the 2% target. For context, the latest eurozone CPI number was over 9%. Follow the link for Euro Price Action Analysis.

At the close and after a volatile session, US indices ended higher. The Dow jumped 0.61%while the S&P 500 had a gain of 0.66%. Sectors leading some of the gains were Consumer Discretionary and Healthcare. News of a new GameStop partnership and a Rivian Automotive joint venture boosted the S&P. Technically speaking, levels of 3,886 and 4,018 in the S&P are good to keep an eye on to see what the next move could be.

S&P 500 (ES) Daily Chart

S&P 500 (ES) Mini Futures Daily Chart Prepared Using TradingView

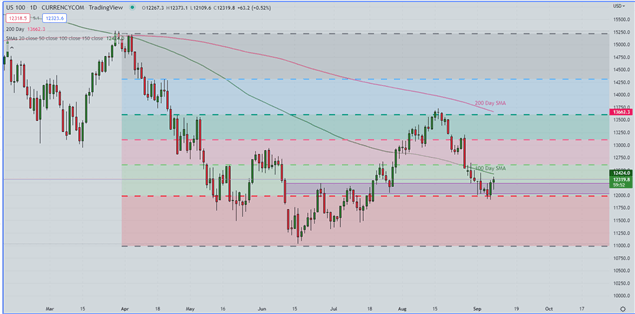

On the other hand, encouraging news from healthcare company Regeneron, which announced positive results from a potential drug, and an outlook upgrade to the Tech company Advanced Micro Devices, supported the Nasdaq 100 and finished with a gain of 0.50%. The index is trying to rebound from an important support zone but struggling with the 100 SMA at the top.

Nasdaq 100 Daily Chart

Nasdaq 100 Daily Chart Prepared Using TradingView

On a side note, it is surprising to see how quickly markets shrug off the prospect of rising interest rates around the world, regardless of the economic slowdown this could bring to already heavily-indebted countries.

Looking ahead: There’s more Fed-speak tomorrow as FED members continue to try to position the market for more aggressive rate hikes. The Fed goes into a ‘blackout window’ on Saturday, meaning no more Fed-speak until after the September rate decision. Next week brings CPI, set to be released on September 13th, and that leads into the big event with the September FOMC rate decision on the docket with announcement due on September 21st.

Recommended by Cecilia Sanchez Corona

Get Your Free Equities Forecast

- Are you just getting started? Download the beginners’ guide for FX traders

- Would you like to know more about your trading personality? Take the DailyFX quiz and find out

- IG’s client positioning data provides valuable information on market sentiment. Get your free guide on how to use this powerful trading indicator here.

—Written by Cecilia Sanchez-Corona, Research Team, DailyFX

[ad_2]

Image and article originally from www.dailyfx.com. Read the original article here.