[ad_1]

(Bloomberg) — It’s a niche trade beloved by retail players and institutional pros that’s paid off handsomely this year: Selling equities just before trillions of dollars worth of options expire.

Most Read from Bloomberg

Yet this time round, the strategy is backfiring in the latest case of a punishing stock market that’s challenging once-reliable playbooks.

Heading into Friday’s $2 trillion options expiration, a monthly event known as OpEx, the S&P 500 has climbed more than 2% this week — despite a drop on Thursday. That’s a departure from the previous nine months, where all but one such episodes saw equities falling. In fact, the losing streak over the six months through September was the longest since 2004.

What underlines the shift in favor of equities of late is debatable. Some attribute it to better-than-feared corporate earnings, depressed investor positioning or a favorable seasonal pattern. Others point to an investor rush to buy bullish options to catch up with a market bounce. Whatever the reason, anyone betting the event would help undercut stocks would have been caught out.

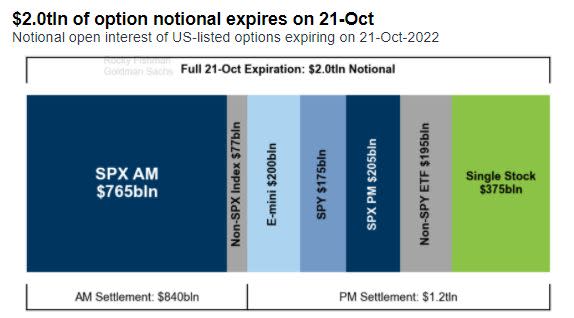

About $2 trillion of options are set to expire, meaning holders will need to either roll over existing positions or start new ones. The event includes more than $1 trillion of S&P 500-linked contracts and $375 billion of derivatives across single stocks scheduled to run out, according to estimates by Goldman Sachs Group Inc. strategist Rocky Fishman.

The S&P 500 fell 0.8% Thursday to close at 3,665.78, erasing an earlier 1.1% gain, as bond yields marched ever higher.

Daily reversals have become more frequent as narratives flip between a Federal Reserve-induced recession to still-strong economic growth that may pave the way for a risk rebound after all. Add market fireworks caused by the ever-growing industry of options buying and selling, and things are looking dicey out there.

One controversial theory holds that the rise of options trading has made stocks the hostage of their own derivatives, at times helping amply market moves.

Options “have become a bigger part of the puzzle,” said Chris Murphy, co-head of derivatives strategy at Susquehanna International Group. “It contributes to the latest market volatility, but not a leading factor.”

Heading into Friday’s event, investors were retreating from stocks in droves. Retail investors, for instance, sold stocks for four straight weeks, according to an estimate by JPMorgan Chase & Co. based on public data on exchanges. Meanwhile, hedge funds tracked by the firm last week saw their net leverage — a measure of risk appetite that takes into account their long versus short positions — sitting at the bottom of a range since 2017.

Such defensive stance, along with the market’s historic tendency for a year-end rally, has prompted Elan Luger, JPMorgan’s head of US cash trading, to shift from the sell-the-rally mode to buying the dip despite all the reservations over the macro backdrop.

“Seasonality is now on your side, retail flows seem to have stabilized, and every hedge fund and mutual fund is positioned defensively,” Luger wrote in a note. “There most certainly seems to be more activity/pain on moves higher than on moves lower which suggests to me nets may come up into weakness to protect yearend relative performance.”

While this represents a tactical shift, Luger remains cautious about piling in at this stage. In fact, he considers the S&P 500 above 3,800 “a sale.”

Brent Kochuba, founder of SpotGamma, agrees that the 3,800 level will likely put a lid on the index. There are fairly large put positions set to expire Friday, and as the value of these contracts decays, market makers who had shorted stocks to balance their exposures would need to unwind their positions, acting as a tailwind to the cash market, he said.

“The reason we look for a top at 3,750-3,800 is that’s where our model shows put-decay no longer fueling markets,” Kochuba said. “After OpEx, we think the market will break from this 3,700 area due to the concentration of positions expiring in this area. We are giving an edge to markets breaking lower, to the 3,600 line as we do not see traders electing to purchase call options at this time.”

Most Read from Bloomberg Businessweek

©2022 Bloomberg L.P.

[ad_2]

Image and article originally from finance.yahoo.com. Read the original article here.