[ad_1]

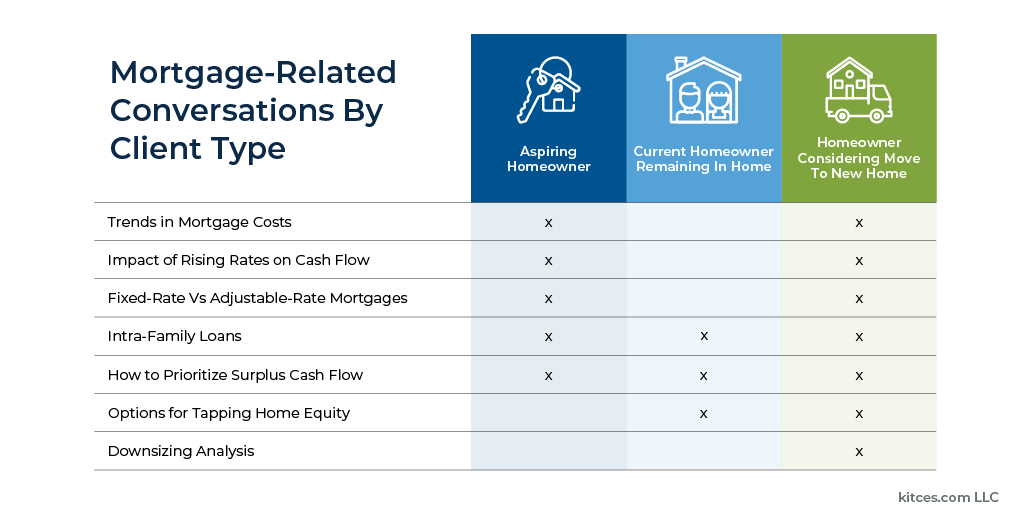

Leading up to 2022, financial advisors and their clients had grown accustomed to a relatively low mortgage rate environment. In fact, until earlier this year, the average 30-year fixed mortgage rate had stayed below 5% since 2010 (and below 7% since 2001). But as the Federal Reserve has sought to raise interest rates this year to combat inflation, mortgage rates have reached higher levels not seen in more than 20 years, with 30-year fixed mortgages reaching an average of 6.9% in October 2022, twice the 3.45% average rate in January.

While the plight of today’s first-time homebuyers facing higher mortgage rates has attracted much media attention (deservedly so, as the monthly payment on a 30-year fixed mortgage for the median-priced home in the U.S. increased by nearly $1,000 in the past year), higher interest rates can affect financial planning calculations for current homeowners as well. For instance, higher interest rates have raised the borrowing costs for those looking to tap their home equity through a home equity loan or a Home Equity Line Of Credit (HELOC), and older homeowners considering a reverse mortgage will also be subject to higher interest rates.

At the same time, higher interest rates can present opportunities for some individuals. For example, those who are interested in making an intra-family loan could generate more income from the higher Applicable Federal Rates (while the loan recipient benefits from a rate significantly lower than standard mortgage rates). In addition, many current homeowners could have mortgages with rates lower than the ‘risk-free’ rate of return now available on U.S. government debt, which has risen alongside broader interest rates (perhaps changing the calculus of whether to pay down their mortgage early). And current homeowners with significant equity could consider downsizing and buying a smaller home in cash, potentially benefiting from a less-competitive housing market while not having to take out a mortgage at the current rates.

Ultimately, the key point is that a higher interest-rate environment affects not only homebuyers looking to purchase a home for the first time but also those who are current homeowners. Further, given that a home can be considered a consumption good (that often comes with emotional attachments) as well as an asset on the homeowner’s net worth statement, advisors can also add value by helping clients explore their home-related goals and assessing the financial tradeoffs of purchasing a more or less expensive home with a mortgage in a higher rate environment (or, if they have the means, whether buying a home in cash might be appropriate!). Regardless of whether a client is an aspiring first-time homebuyer or considering downsizing in retirement, advisors can add value by helping their clients navigate higher mortgage-rate environments!

[ad_2]

Image and article originally from feeds.feedblitz.com. Read the original article here.